.svg)

Read TL;DR

- Pass-through costs definition: Third-party expenses incurred for a specific client or project and billed to the customer at or near cost.

- Pass-throughs are not core operating costs and should be separated from core revenue for analysis.

- Under ASC 606, whether pass-throughs are shown gross or net depends on principal vs agent treatment, even when the economics are similar.

- Large pass-through volumes inflate your reported revenue and distort the true revenue growth of your company.

- Clear policies and the right system configuration are key to helping your team manage pass-through costs effectively.

Pass-through costs are expenses that show up in your records when you act as an intermediary. You pay a third party on your customer’s behalf and charge that amount (sometimes with a markup or handling fee as per your policy) to the customer.

Once you learn to identify pass-through costs, you’ll see that the transactions are pretty straightforward, but their implications on your financial statements can make revenue and margins less meaningful, especially if you have a lot of them.

They are very common for agencies, consultancies, and project-based service firms, which often incur and bill significant third-party expenses on behalf of customers. For companies that sell mostly products, pass-throughs are much less common.

Summary

Pass-through costs, also referred to as flow-through costs, are incurred on behalf of a customer and charged to them at the time of billing at near or actual costs. They typically relate to third-party goods or services tied to a specific client or project.

In this guide, we explain how pass-through costs impact your revenue and how your team can forecast and report them without distorting financial performance. We also look at some revenue recognition basics to help you steer clear of issues during the audit.

What are pass-through costs?

Pass-through costs are expenses incurred by your business on behalf of a specific customer, which are billed back to them at or near cost.

The company isn’t selling the items for which pass-through costs are charged to the customer, at least in the economic sense. It’s just recovering cash paid to a third party that the customer was supposed to spend. The primary goal is reimbursement; any margin is typically explicit and secondary.

Agent vs. principal: how pass-through costs are classified

Understanding your company’s role in every transaction is key to distinguishing pass-through costs from other types of expenses.

A company acts as an agent for pass-through costs when it purchases third-party goods or services specifically for a client’s project, passes those costs through without markup, and is simply reimbursed.

In this case, the company does not add substantial value to these transactions, and the risk and reward primarily remain with the client. These costs are billed separately and do not contribute to gross margin, but are accounted for as “other income” or offsetting within financial statements.

By contrast, a company acts as a principal when it integrates external costs into its core deliverables—such as bundling third-party products or subcontracted labor into a full-service offering.

Here, the company takes on primary responsibility, combines outside costs with its own value-add, bears more risk (such as quality or delivery issues), and recognizes the entire amount as revenue, with corresponding direct costs deducted from gross profit.

Why is this distinction important?

Correctly identifying your company’s role determines how revenue and expenses are recognized and reported, which directly impacts forecasts, operating metrics, and performance evaluation.

Whether you are acting as an agent or a principal in the transaction directly affects how you report third-party costs and shapes how you classify, forecast, and analyze your financial performance.

Pass-through costs vs. OpEx (non‑billed)

Pass-through costs are always tied to a particular client and are recoverable from that client, usually on a separate line in the invoice. In contrast, operating expenses (OpEx) are general business expenses that cannot be charged to a specific customer.

So, if you’re wondering if a cost is pass-through or OpEx, ask yourself:

Is this cost incurred as part of delivering a service or product for a specific client or project, and can I bill it directly back to that client—separate from the main price of my own services?

- If yes, it’s a pass-through cost.

- If not, ask yourself the next question.

Is this cost a general, recurring expense required to run my business (e.g., office rent, internal software licenses, routine business travel, electricity, etc.)—one that isn’t tied to any single client, and cannot be billed directly to a client?

- If yes: It’s an operating expense (OpEx).

- If not, re-examine the cost; it may belong to another category (e.g., direct cost of sales as principal).

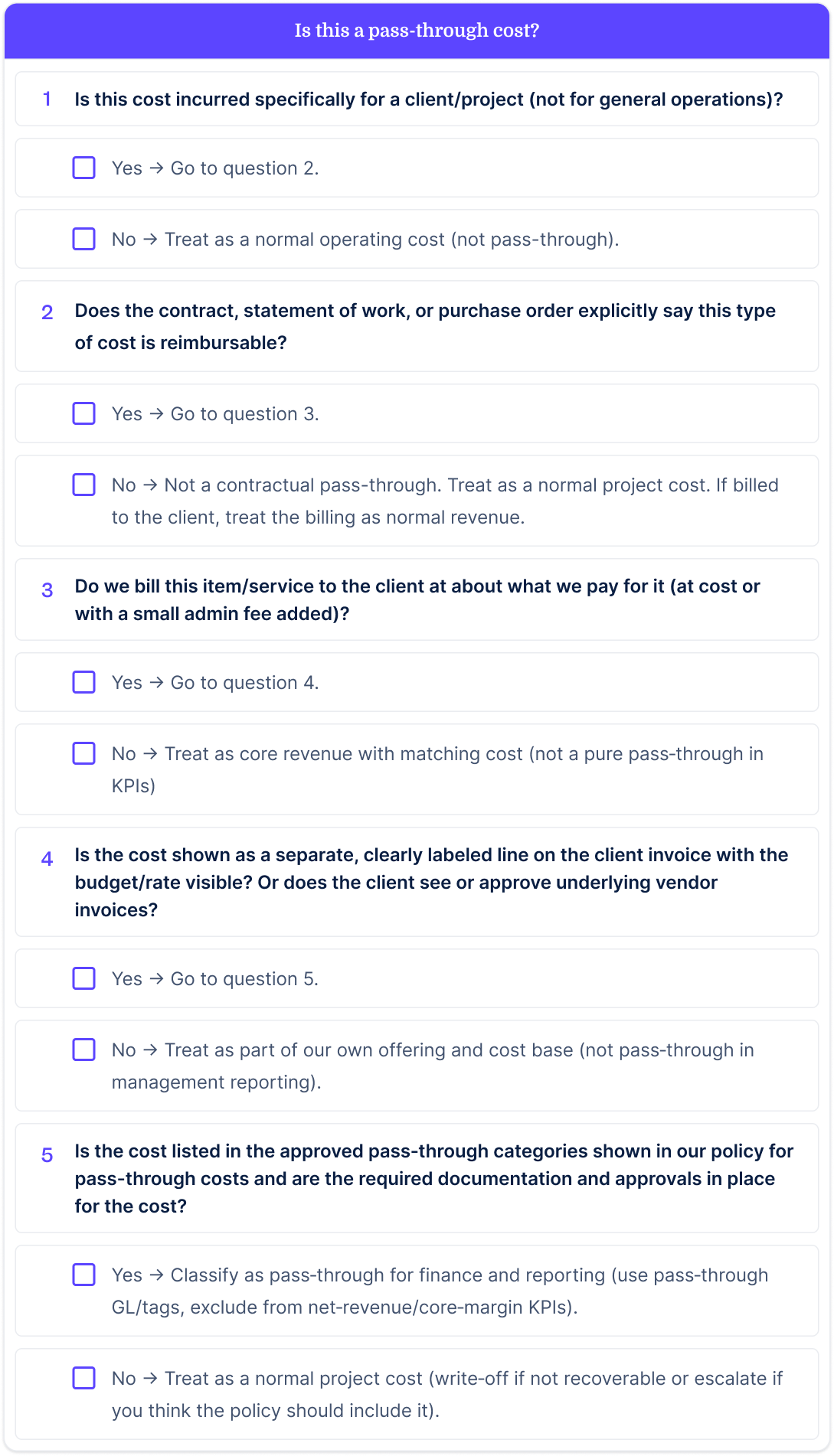

Rules of thumb for determining whether a cost is pass-through

A cost is likely a pass-through cost if most of the following are true:

- It’s incurred for a specific client or project, not general operations.

- The contract explicitly allows for reimbursement of these costs.

- It appears as a separate line item in the bill.

- Your company’s role is similar to that of a broker or agent in the transaction.

- The client can track or approve the amount spent on pass-through transactions.

On the other hand, a cost is usually not a pass-through when:

- It’s not contractually reimbursable as a pass-through item.

- It’s bundled into your own pricing and not shown separately to the client.

- The cost includes a meaningful markup and is one of the ways for you to earn a margin on core revenue.

- Your company is clearly acting as a principal, selling its own product or service and taking on all the performance and pricing risk.

Here's a handy cheat sheet to help you identify pass-through costs:

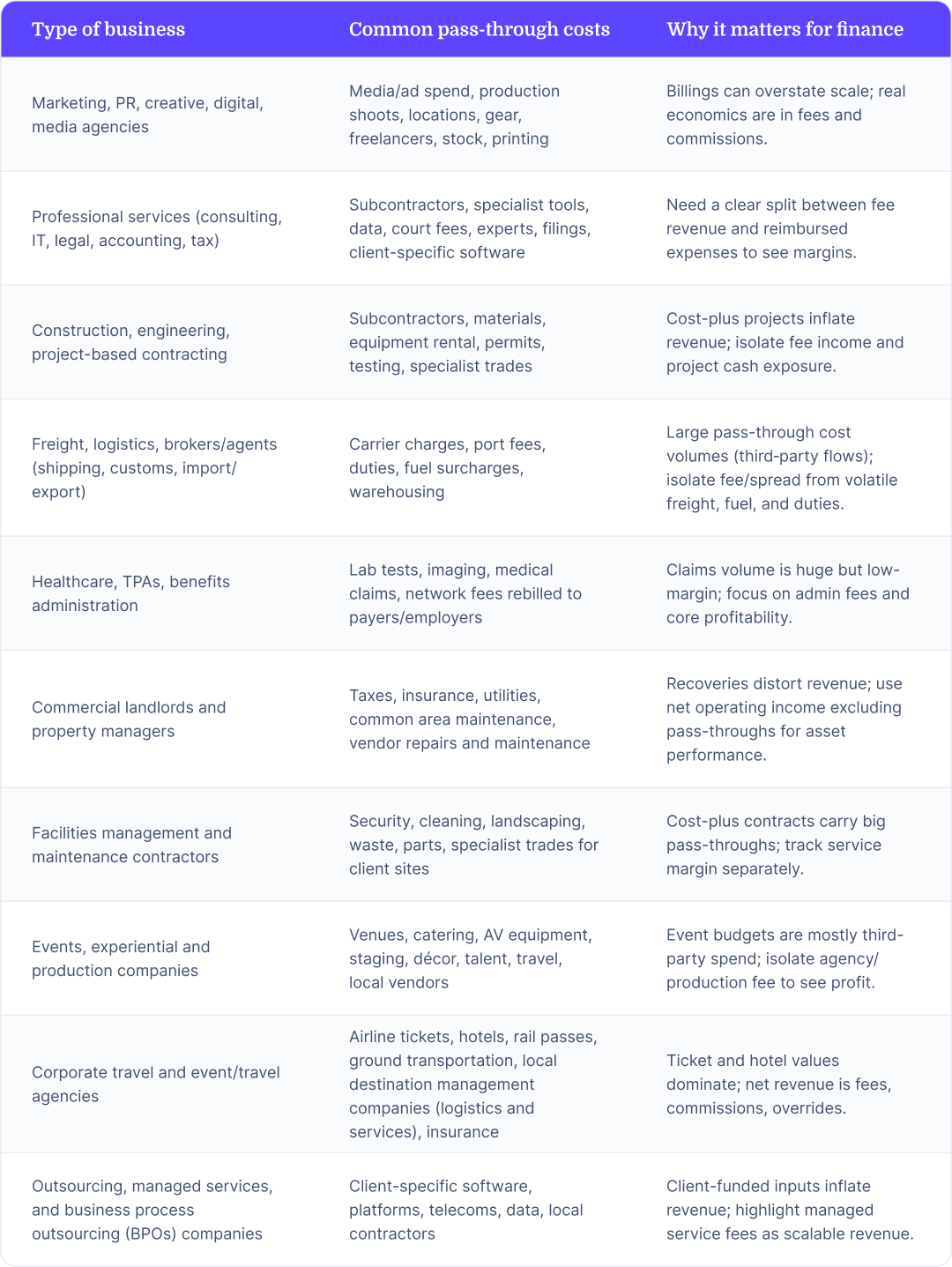

What kinds of businesses have pass-through costs?

Pass-through costs appear more frequently in industries where companies manage or pay a third party on behalf of customers. Here are some common pass-through cost examples and why they matter for finance teams.

Why do pass-through costs matter for finance?

Pass-through costs directly affect revenue recognition and forecasting accuracy. If you don’t isolate them, they’ll inflate reported revenue and distort the real economics of your business.

Here are some key reasons why you need to pay attention to pass-through costs:

Pass-through costs and revenue recognition

According to ASC 606 (revenue recognition), you’re a principal if your company controls the goods or services and an agent if you’re merely arranging them for your customer.

To comply with the practices for ASC 606 pass-through costs, principals must report gross revenue, while agents must report net revenue. In either case, it’s important to track both net and gross revenue if you want to analyze revenue growth accurately.

Forecasting and planning

Pass-through volumes can be volatile. Mixing those numbers with your core revenue and using that figure to forecast revenue for future periods gives you a distorted view of potential revenue growth. To avoid this, always separate pass-throughs before forecasting revenue.

Pricing and contract negotiation

Costs passed through at cost shift the risk of inflation and FX risk to the client, while bundled costs shift those risks to the company. As you can imagine, this distinction affects how you evaluate the economics of your deal and structure the fees, whether that’s through commissions, markups, management fees, or fixed pricing.

Risk of misclassification

Misclassifying pass-through costs leads to inaccurate management reporting, non-compliant revenue recognition, audit issues, and disputes with customers over what’s reimbursable.

Best practices for avoiding common pitfalls with pass-through costs

Pass-throughs can create three big problems for finance teams: they distort your metrics and KPIs, they mislead leadership about real performance, and they create incentives for teams to chase high-volume, low-margin work.

The five practices below will help you eliminate those distortions at every level—from your GL structure to your forecasts to executive dashboards.

1. Collaborate with accounting teams

Finance and accounting teams have different goals when it comes to pass-through costs. Accounting focuses on correctness and compliance, but your priority is insights that help you make better decisions. Working with your accounting team is essential to accurately track pass-through costs.

Why it matters

If your accounting team treats pass-through costs differently from the method described in the contract, you'll spend hours every month trying to identify and strip out pass-throughs manually in spreadsheets.

How to avoid the pitfalls

The best way to achieve your goals as the finance team is to isolate pass-through costs in dedicated GL accounts or account groups rather than mixing them with core revenue or operating costs.

To make sure everyone wins, work with your accounting team to make pass-through costs clearly identifiable in the ledger. Ask them to provide:

- Clear reporting mappings where pass-through items appear as separate lines

- Dedicated accounts or account ranges for pass-through costs and reimbursed revenue

Once you do this, you’ll have accurate margin data (that excludes pass-throughs) and unit economics that reflect true value-add. You’ll be able to benchmark across teams and peers using net revenue, and build forecasts faster with pass-throughs modeled separately from core pricing.

When reporting, just make sure you always show reported (gross) and net revenue side-by-side with clear labels to help your leadership understand both the volume story and the economic story.

2. Align incentives to net revenue and margin

Bonuses, commissions, and other performance-based incentives should be tied to net revenue and margin, not gross billings that include pass-throughs. If you need to use gross billings to track scale or market share, pair them with explicit margin targets so your team isn't rewarded for pushing volume alone.

Why it matters

Incentives tied to gross billings that include pass-throughs can push your sales and delivery teams toward high-volume, low-margin activity.

How to avoid the pitfalls

Explicitly define "qualifying revenue" or "commissionable revenue" as the net of pass-throughs in your compensation plan documents.

Run test scenarios with finance and sales leadership using recent deals to make sure the new structure rewards the behavior you actually want—margin and profitability, not just volume.

If you're keeping gross billings metrics for market positioning or scale tracking, create a paired scorecard that shows both gross billings and net revenue/margin targets together, with clear thresholds so no one can hit their number on volume without delivering profit.

3. Refine KPIs to eliminate pass-through distortion

It’s important to exclude pass-through costs from the formulas your systems use to compute core KPIs like contribution margin, revenue per FTE, customer LTV, and CAC.

You can still track pass-through volumes separately for operational context—just don't let them feed into the metrics that measure real performance and profitability.

Why it matters

Your dashboards will tell a story that doesn't match your P&L. And your leadership will end up making strategic decisions, resource allocations, and growth commitments based on metrics that don't reflect true economic performance.

How to avoid the pitfalls

Start by auditing which KPIs and dashboards currently use gross revenue or total billings as inputs. Recalculate them using net revenue (revenue minus pass-throughs) as your base. Update your planning and BI tools to automatically flag or separate pass-through flows so they don't contaminate core metrics by default.

Build dashboard views that show both gross and net versions of key metrics side-by-side during the transition so stakeholders can see the difference and understand why you're making the change.

4. Model pass-through costs separately and run scenarios

It’s best to model your pass-through costs based on their own drivers—things like client budgets, project scope, usage volumes, or external rates—as opposed to a straight percentage of core revenue. You should also forecast core revenue and pass-throughs separately, then add them up to see the full picture.

Once you've got separate models, run scenarios that isolate what happens when pass-throughs move independently:

- What if pass-through volume spikes but core revenue stays flat?

- What if core revenue grows but pass-throughs stay stable?

If there's a real connection between pass-through volumes and your core business (common in project-based work or budget-linked models), call that out explicitly rather than pretending they're totally independent.

Why it matters

Pass-through costs are usually volatile and driven by things you don't control. If you lump them in with core revenue, your forecasts will swing wildly for reasons that have nothing to do with your core business.

How to avoid the pitfalls

Start by pulling out pass-through volumes from your current financial data and getting clear on whether you're billing them at cost or adding a markup.

Build separate forecast drivers for pass-throughs (like "client media budget assumptions" or "expected freight volume") and for core revenue (like "service fees," "active clients," "pricing"). Add them together for your total reported revenue, but always show them side-by-side so leadership can see both the volume story and the real economics.

Run at least two scenarios in each planning cycle to show how different pass-through assumptions change your reported numbers without changing your actual profitability. Make sure to flag any real correlation between pass-through activity and core drivers so stakeholders understand when the two actually move together.

Operationalizing governance: policies and system configuration for pass-through costs

Governance and systems are critical to manage pass-through costs consistently and at scale. That means you need to put guardrails around what qualifies as a pass-through and ensure those rules are supported by the tools used to book and report costs. Let’s look at how you can set up governance and systems for pass-through costs.

Build a policy and approval framework

Without a clear policy, similar costs may get different treatment across teams and contracts, and lead to inconsistent reporting and unnecessary issues with customers. So the first step is agreeing on what qualifies as a pass-through in the first place.

When drafting your policy, clearly define which cost categories are eligible and whether you’ll charge a markup or handling fee. Then prescribe a course of action for situations where a cost is incurred without approval or falls outside approved categories. The course of action could be writing off the cost or treating it as a normal project cost.

Configure your ERP and planning tools

Configuring your ERP and planning tools helps you enforce the policy you created in the previous steps.

Let’s look at the ERP or accounting system first because that’s usually the system of first record. Make sure all transactions in your system of record are tagged as pass-through or non-pass-through and that each transaction is linked to a specific client, contract, vendor, or project.

Once you’re done, configure your planning and reporting tools. These tools can pull pass-through costs and net revenue separately from your system of record, so it’s usually easy to show both of them as separate line items.

The specific methods of configuration depend on the specific system you’re using, but the end goal is the same.

Key takeaways for finance leaders

Pass-through costs aren’t exactly troublesome, provided you define them clearly and don’t mix them with core revenue. The problem? It’s hard to track them manually, especially at scale, but that’s exactly where platforms like Drivetrain help.

Drivetrain makes it easier to deal with pass-through costs. It offers granular visibility into pass-through drivers and the ability to toggle between gross and net views. It also offers scenario modeling capabilities that allow you to assess how changes in third-party spend affect margins and unit economics.

If you’re looking for a better way to track and report pass-through costs, book a demo to learn more about how Drivetrain can help.

FAQs

Media and ad spend, freight and shipping charges, subcontractor fees, travel billed to clients, lab tests, permits, and utilities costs passed on to tenants are all examples of pass-through costs.

Always forecast pass-through volumes separately from core revenue and be explicit with your margin assumptions because pass-through transactions carry little or no profit. Just following these basic rules will help you avoid errors and confusion in your forecasts.

Recognition under ASC 606 depends on whether your company is acting as a principal or agent. If you’re acting as an agent, recognize revenue net of pass-through costs. On the other hand, if you are the principal, the cost is not a pass-through; it is a cost of sales.

Common examples of businesses that deal with pass-through costs are agencies, professional services, construction, logistics, healthcare administration, facilities management, real estate, and event management. Basically, any business that manages third-party spend for customers, either by choice or industry convention, will need to deal with pass-through costs.

They’re closely related but technically different. Reimbursable expenses are one type of pass-through cost, but pass-through costs can also include larger third-party spend like media and subcontracted services, not just employee expenses.

Note that in some sectors (e.g., construction, media, etc.) the terms “reimbursable” and “pass-through” may be legally or contractually conflated.

Contracts help because you can clearly define which costs are reimbursable and whether you or the customer will bear the risk of inflation or fluctuations in FX rates. Separating pass-through costs from fees and using transparent pricing terms is the best way to steer clear of disputes with customers and minimize volatility in margins.

Like this article?

.svg)

.svg)

.svg)