.svg)

Read TL;DR

- Contracted ARR combines your current ARR with contracted revenue that hasn't yet gone live.

- It's a point-in-time metric that shows your total committed recurring revenue, making it essential for valuations, forecasting, and resource planning.

- The main calculation challenge is normalizing multi-year contracts with varying annual values: first-year values are most conservative, averages work for long-term planning, and exit-year values are highly discouraged because they can materially overstate current revenue potential.

- Track your contracted ARR to ARR conversion rate to ensure contracted revenue is actually converting. Document your methodology and maintain clean data across systems.

When investors evaluate a SaaS company, they aren't satisfied with just knowing what you're earning today; they want to go deeper and see what's already locked in for tomorrow. The metric they use to determine this is contracted annual recurring revenue (contracted ARR). A strong contracted ARR signals stability, predictable revenue that reduces risk. It demonstrates a growth trajectory before that growth hits your P&L, which, for SaaS businesses, can lead to higher valuations and better terms.

The growing interest in contracted ARR reflects a broader shift toward predictable revenue as the currency of SaaS valuation. While ARR tells where you are, contracted ARR tells where you're headed.

Summary

Contracted annual recurring revenue represents the total annualized value of all recurring revenue in existing customer contracts, including those that have been signed but haven't yet started generating revenue. Contracted annual recurring revenue offers SaaS companies a forward-looking measure of financial health, capturing not just current performance but guaranteed future revenue that's waiting to go live.

This guide provides an in-depth discussion of how to calculate contracted ARR step by step, including methods for normalizing multi-year contracts, which can be particularly challenging. We'll also discuss other key metrics to track that reveal whether your contracted ARR is converting as expected and how to avoid the most common mistakes in tracking and reporting.

What is contracted annual recurring revenue?

Contracted annual recurring revenue (contracted ARR) measures your total recurring revenue potential by combining what you're already earning from customers who are actively using your product with the committed revenue in contracts with those who are currently onboarding or haven't started yet. Think of it as ARR plus the committed future revenue sitting in your pipeline. Contracted annual recurring revenue is often referred to as committed revenue, contracted ARR, or CARR.

The key distinction between contracted ARR and other revenue metrics is that it includes contracted future revenue that hasn't yet been realized. Let's say a customer signs a deal in October that doesn't go live until January. That revenue won't show up in your ARR until they're actually using the product, but it most certainly counts toward contracted ARR.

This makes contracted ARR a “point-in-time" metric, similar to a balance sheet item. You're essentially looking at a snapshot of where things stand on a specific date. Revenue, by contrast, is an income statement metric. It reflects a period of time and only captures revenue for services already rendered.

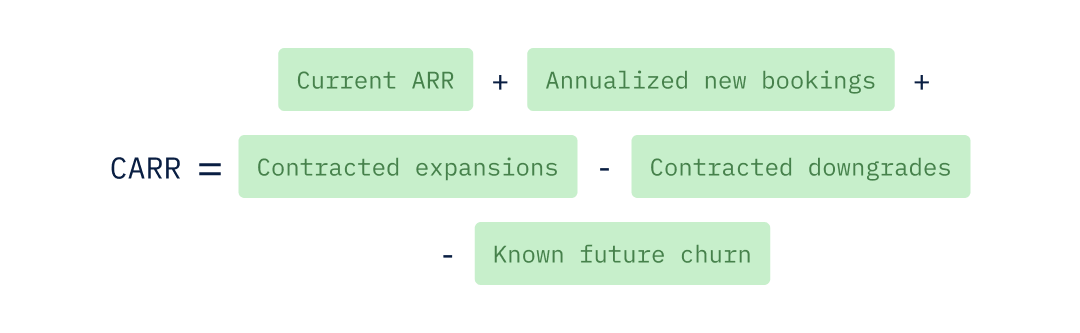

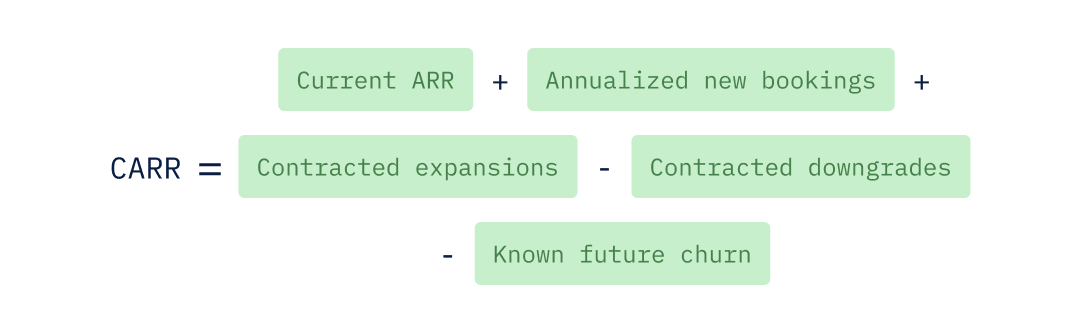

Here's the formula:

In the formula above, current ARR is revenue from contracts that are live, meaning the customer has been fully onboarded and is actively using your product.

Annualized new bookings reflects the revenue from signed contracts that aren't live yet. These could be multi-year deals or contracts with delayed start dates. Think of it as "the ink (on the contract) is dry", but the customer hasn't started using the product.

Contracted expansions, contracted downgrades, and known future churn represent revenue gained or lost from existing live customers. One nuance worth noting is that "contracted" here can mean either that a customer has indicated an intention to upgrade or downgrade, or that the changes have actually been formalized in the contract. The latter is more reliable for forecasting. "Known" future churn simply means the customer has given notice. You can find a deeper breakdown of these ARR components in our ARR metrics article.

What Contracted ARR doesn't include

Contracted ARR is built to track future growth from "recurring revenue." That means certain revenue streams don't belong in the calculation, even if they're substantial.

This means any one-time revenue stays out, as well as implementation fees and professional services, as these are project-based versus recurring revenue.

Managed services sit in a gray area. This revenue can technically be recurring, which makes it tempting to include. But experts argue against it. The reasoning is sound: Managed services are technically not the core product or IP. They also scale differently from core product subscriptions and can muddy your view of true revenue growth attributable to your product.

Trial subscriptions don't count, either. Simply put, until a customer converts to a paid contract, there's no committed ARR.

The ARR lifecycle

Tracking revenue for the purposes of calculating contracted ARR requires an understanding of each stage in the revenue lifecycle. Here's how it works:

Stage 1: Contract signed: The ARR gets recorded in annualized new bookings. You have a commitment, but the customer isn't using the product yet.

Stage 2: Customer goes live: The ARR shifts from annualized new bookings to Current ARR. Now, they're onboarded, active, and generating recognized revenue.

Stage 3: Ongoing service delivery: The ARR stays in Current ARR for as long as the customer remains active.

Stage 4: Contract ends or customer churns: The ARR gets removed from Current ARR.

Why is tracking contracted annual recurring revenue important?

Contracted ARR offers a forward-looking measure of financial health. By including all guaranteed future earnings, not just what's currently active, it goes a step further than ARR, painting a more complete picture of revenue potential. This makes forecasting more effective and helps teams identify where recurring revenue growth is actually coming from.

While contracted ARR isn’t typically used as a valuation anchor, investors consider it supporting evidence of the true revenue potential of a SaaS company over the next few years.

That said, the overall importance of tracking contracted ARR can vary based on how your business operates. It may not be useful in all contexts.

CARR vs. ARR

ARR shows what’s live today; contracted ARR shows what’s contractually coming next. Two companies with the same ARR can look very different once signed-but-not-live revenue is considered.

Both metrics matter in valuation, but contracted ARR adds forward-looking context for forecasting and resource decisions. Monthly equivalents (MRR and contracted MRR) follow the same logic, with finer granularity. The table below provides a comparison of ARR and contracted ARR for more context.

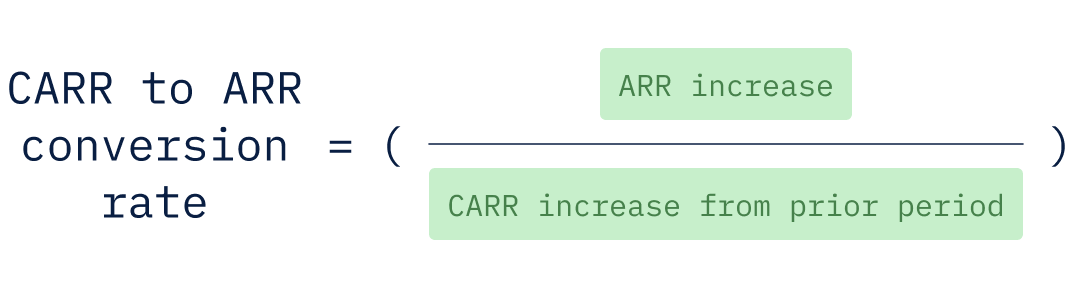

The contracted ARR to ARR conversion rate

The contracted ARR to ARR Conversion Rate is an often-overlooked metric that can help you evaluate how efficiently you're turning contracted revenue into actual recognized revenue. In other words, how effective are your onboarding and customer success processes at getting signed customers up and running live?

Here's the formula:

Contracted ARR means nothing if it never converts to recognized revenue. You can book deals all day, but if customers stall during onboarding or cancel before they even go live, that contracted ARR will never be realized. This ratio reveals whether your contracted ARR growth reflects real momentum or an underlying problem with implementation.

Because contracts go live at different speeds, changes in ARR don’t line up perfectly with when the contracted ARR was booked. That means the ratio can swing from period to period due to timing alone. So, it’s not always an indicator of problems with getting new customers onboarded.

Tracking the trend in your contracted ARR to ARR conversion rate over time, can help to smooth out those timing effects and provide a clearer picture of whether conversion performance is actually improving or deteriorating.

Here are a few red flags to watch for:

- Contracted ARR increasing but ARR staying flat: You're signing deals but not getting customers live. That points to implementation problems, either capacity constraints, process inefficiencies, or product issues that are slowing down onboarding.

- Conversion rate declining over time: If it's taking longer to convert contracted ARR to ARR than it used to, it may be the result of increasing complexity. Maybe you're moving upmarket, adding integrations, or your product has grown more complicated to deploy.

- Long-tail contracted ARR that never converts: Some contracted revenue just sits there indefinitely. That's a problem with the quality of your bookings. Your sales team may be closing deals that aren't a good fit, or contracts are being signed with customers who aren't ready to implement.

- High contracted ARR driven by short post-trial commitments: Some companies give customers the option of canceling their contract after a trial (often three months). This appears to be a trend with AI SaaS companies in particular. The problem here is that these deals inflate contracted ARR at signing but frequently churn before going live or reaching steady-state usage. In these cases, the contracted ARR never translates into ARR.

What is a good contracted ARR to ARR conversion rate?

The truth is, there's no universal benchmark here. Conversion patterns vary based on implementation complexity; a company with 30-day onboarding will look completely different from one with 6-month enterprise deployments.

The best approach is to establish your own baseline. Start tracking:

- Your average implementation timeline

- Historical conversion rates by cohort

- How these metrics change over time

Once you have that baseline, you can work with it. You'll be able to evaluate whether current performance is consistent with historical patterns, more accurately predict the timing of contracted ARR to ARR conversions, and determine whether your conversion rates are stable or improving quarter over quarter.

Booked vs. contracted ARR

Bookings, or booked ARR, represents the total value of new contracts signed in a given period. While it has an impact on revenue, bookings is a sales performance metric—a measure of deals closed, regardless of when that revenue will go live or when it is recognized.

Bookings are an input that flows into contracted ARR. When a contract gets signed, it enters contracted ARR as part of annualized new bookings (one of the variables in the contracted ARR equation). From there, once the customer goes live, the revenue from that new contract eventually converts to ARR, another variable in the contracted ARR equation.

The table below provides a summary comparison of bookings and contracted ARR for more context:

How to calculate contracted ARR: step-by-step methodology

Here's the contracted ARR formula again for reference:

Now, let's walk through how to actually calculate each component.

Step 1. Decide the reporting date

Pick your reporting date first. All amounts and proration calculations flow from this date. Everything in contracted ARR is measured as of this specific point in time.

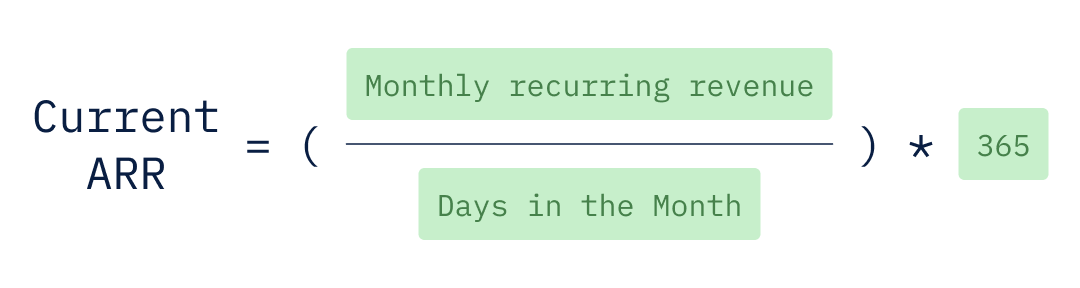

Step 2. Calculate the Current ARR component of contracted ARR

Current ARR represents your recurring revenue run rate at a specific point in time. It is independent of GAAP revenue recognition, which governs when revenue is recognized on the P&L based on the satisfaction of performance obligations, not when cash is collected.

Instead, ARR reflects the annualized recurring value of active subscription contracts based on current contractual rights and obligations—that is, what the customer is entitled to receive and what the company is entitled to bill for on a recurring basis.

It is independent of GAAP and IFRS standards for revenue recognition timing, which are accounting principles that pertain to when you actually receive the revenue from the customer and book it on your P&L. In contrast, ARR reflects the annualized recurring value of active subscription contracts based on current contractual rights and obligations, whether payment has been received or not.

For the purposes of calculating contracted ARR, a customer’s ARR stays in Current ARR as long as the subscription is active and unchanged. You would only need to update the ARR for that customer if the underlying subscription terms change. Changes can include activation (the customer is onboarded and begins paying), churn, expansion, downgrades, or the prices in the contract are amended.

There are three approaches you can use here:

Simple method

Why use this method? It's the easiest calculation, requiring minimal analysis and no separate subscription databases.

You get a direct tie to your P&L using actual recognized revenue from financial statements, with a straightforward audit trail that reconciles directly to GAAP financials. It reflects actual economic activity—what customers paid during the period—which is directionally accurate for valuation and investor reporting.

This method works well for stable, mature companies with minimal month-to-month changes. It's also a good fit for small finance teams with limited resources, internal reporting where directional accuracy matters more than precision, and monthly board updates that don't require investor-grade numbers.

If your revenue patterns are predictable, most subscriptions start on the first of the month, and churn is low enough that differences between methods are immaterial, this approach gets the job done. It's also practical for companies without sophisticated billing systems that can generate point-in-time snapshots.

Prorated method

Note: "Days in the month" should reflect actual calendar days, not an average or fixed number.

This method provides comparability across months of different lengths and removes calendar artifacts from your numbers. It's useful for mid-quarter calculations reflecting partial periods and gives you a true run rate rather than period-specific recognized amounts.

This works well for high-growth companies where month-to-month changes are significant and precision matters. It's also the right choice when reporting to investors who want precise figures or when calculating metrics mid-period.

End-of-period method

This method is forward-looking, capturing your run rate rather than past recognized revenue. You get a true point-in-time snapshot that answers, What is our business worth today? instead of, What did we earn last month?

This aligns with how investors value businesses—based on current state, not historical recognition. The metric isn't distorted by when revenue was recognized during the month, and it's easier to audit since it's based on contract inventory at a specific date, verifiable from subscription records.

The end-of-period method is ideal for high-velocity sales environments where you're adding and churning customers constantly. Use it for investor reporting and fundraising to show current momentum, or when significant intra-month volatility means end-of-month state differs materially from the average.

It's also the right choice when recent momentum matters—emphasizing late-month wins or de-emphasizing early-month churn—and during valuation discussions where point-in-time metrics drive deal terms.

This method works best with clear contract start and end dates aligned to specific calendar days.

Most companies calculate contracted ARR at standard intervals: monthly, quarterly (March 31, June 30, September 30, December 31), or annually. The "month-end date" in the formula is typically your reporting date.

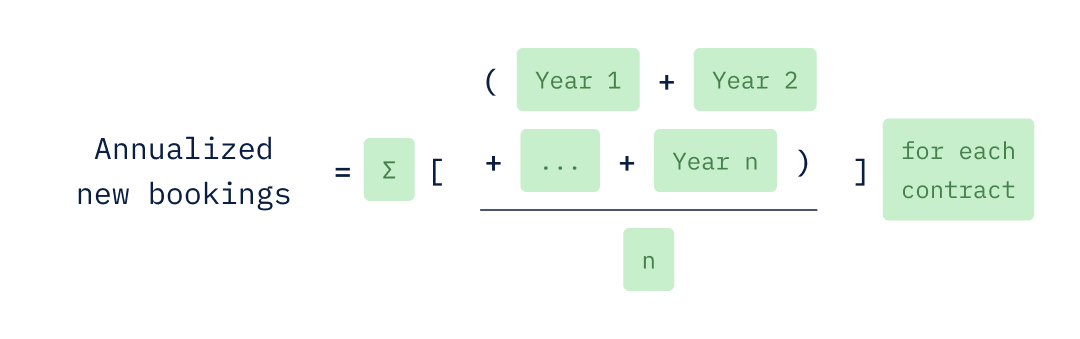

Step 3. Calculate the annualized new bookings component of contracted ARR

Here's where things get tricky. One of the hardest parts of calculating contracted ARR is figuring out how to value multi-year contracts where the annual commitment changes from year to year.

It is well-known that enterprise deals often include long ramp periods, pilot phases, or committed growth schedules, where a customer commits to future increases in subscription spend or usage. With these kinds of contracts, the recurring revenue in year one might look nothing like year three.

Take a three-year contract that specifies $100K in year 1, $200K in year 2, and $300K in year 3. Since contracted ARR represents your annual recurring revenue run rate, you have to choose which year's value to use.

This challenge primarily affects annualized new bookings, where complex deal structures are most common and represent the largest volume of forward-looking contracted ARR additions. It can also apply to contracted expansions when customers commit to multi-year upsell schedules, phased seat rollouts or scheduled tier upgrades, for example, though this happens less frequently.

Contracted downgrades and known future churn typically don't require normalization because they're usually discrete events with specific dates and known amounts. Scheduled multi-year reductions are theoretically possible, but rare in practice.

Normalization methods for multi-year contracts

There are two primary methods for normalizing multi-year contracts. Businesses should choose and document one primary approach for reporting to stakeholders. Many SaaS companies use the average method for stable reporting. Others use the first-year approach for conservatism. The key is to be transparent, whatever method you used to normalize the annualized new bookings for your contracted ARR calculation.

Note that the examples below focus on new bookings only because that’s where normalization is needed and has the biggest impact.

Here are the two approaches for estimating the contracted-but-not-yet-active recurring revenue that gets added to ARR:

- First-year contracted value approach: Uses the contract value billable in the first year of the multi-year contract.

- Average annual contracted value (ACV) approach: Averages the contracted ARR across the full term of the contract.

Each approach is simply a different policy choice for normalization. However, each can have significant implications depending on how your contracts are structured. We'll examine these implications in more detail below.

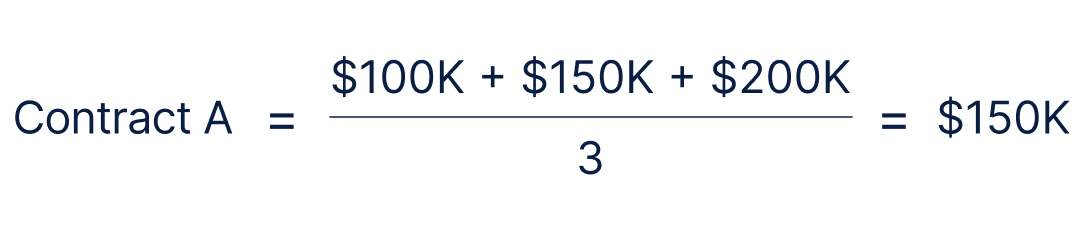

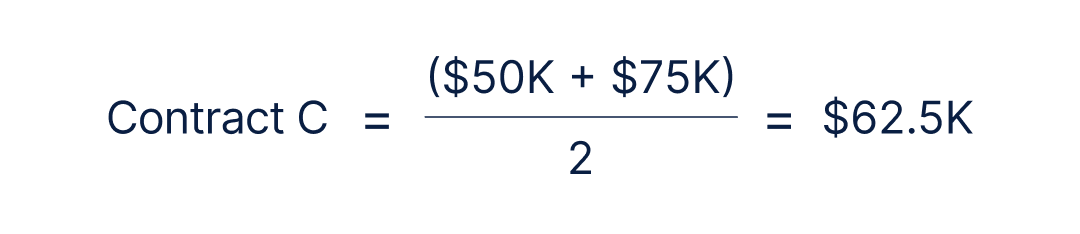

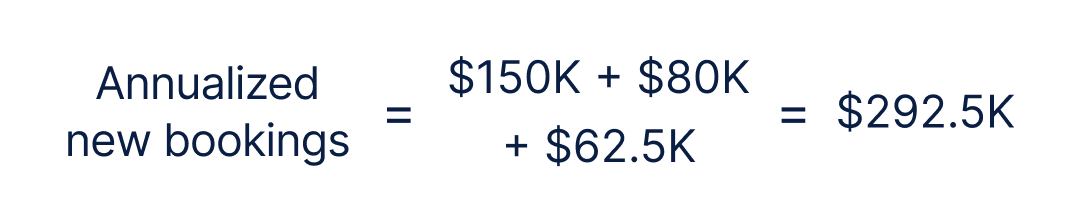

First, here's the new bookings data we'll use for our example calculations:

How bookings and contracted ARR differ in what they measure, the revenue they include, and how to interpret gaps between them.

First-year contracted value

This is commonly used as the default when reporting contracted ARR to the board or investors. It provides the most conservative and accurate view of near-term revenue because it aligns with what will actually hit the P&L in the next 12 months.

That conservatism reduces the risk of investor disappointment when contracted ARR doesn't convert to recognized revenue as expected.

For our example calculation, we simply sum the first-year values for Contracts A, B, and C.

Average annual contract value (ACV)

Use this method if your finance team needs to model long-term revenue visibility. It's useful for capacity planning and long-term forecasting because it smooths out the ramp structures in your contracts. Just make sure it's clearly labeled as "Average contracted ARR" to avoid confusion with other calculations.

The bracketed portion of that formula represents the average annual contract value (ACV) for each contract. To calculate annualized new bookings with this method, you must first calculate the ACV for each contract individually, then sum those averages.

Here's what that looks like, using our example data:

How your choice of normalization method for multi-year contracts can impact contracted ARR

The examples below walk through three different types of multi-year contracts for the purposes of calculating your annualized new bookings to feed into the contracted ARR equation. Each example uses a single contract to keep things simple. While we're not ready to calculate contracted ARR yet, the net impact of our results on contracted ARR is the same since annualized new bookings is a fundamental part of the equation.

Scenario 1: Annualized new bookings for a simple multi-year contract

Let's start with a straightforward case: a three-year contract with a $360K total value and equal annual payments of $120K per year.

- First-year contracted value = $120K

- Average contract value = $120K

In this scenario, the annualized new bookings and thus the impact on your contracted ARR would be identical regardless of which normalization approach you use. When payments are flat across the contract term, the method doesn't matter.

Scenario 2: Annualized new bookings with an escalating contract

Now, consider a three-year contract with the same $360K total value, but with escalations built in:

- Year 1: $100K

- Year 2: $120K

- Year 3: $140K

Here are the results from the different normalization approaches we could use:

- First-year contracted value = $100K. This is the most conservative approach to representing revenue potential.

- Average contract value = $120K. This inflates near-term revenue potential somewhat but can be useful for financial modeling.

Using first-year normalization gives you the most accurate picture of what revenue will actually look like in the near term because you know that $100K is the maximum amount possible in the first year.

Scenario 3: Annualized new bookings for a contract with a ramped deployment

This scenario involves a three-year contract with the same $360K total value, but with a phased rollout:

- Year 1: $40K (pilot phase)

- Year 2: $120K (partial deployment)

- Year 3: $200K (full deployment)

Here's what each normalization approach produces:

- First-year contracted value = $40K

- Average contract value = $120K

First-year normalization is a good choice here because it accurately represents implementation risk and timeline. The customer is in a pilot phase, and hence, full revenue is years away.

Using the average contract value would inflate annualized new bookings to $120K. That's three times the actual year 1 revenue and misrepresents near-term potential since that level isn't possible under the contract until year 2.

Additional considerations when calculating the annualized new bookings for contracted ARR

Regardless of whether you're working with annual contracts or multi-year deals, it's critical to avoid double-counting.

If a contract has already gone live and is included in Current ARR, remove it from new bookings. Each contract should appear in either current ARR (if active) or in forward-looking components (if not yet active), never both.

One more thing to keep in mind is that if you're dealing with annual contracts, you don't need to normalize as they're already annualized. Normalization only comes into play with multi-year contracts. And even then, it's only a challenge when those contracts have varying annual values.

As we saw in Scenario 1, multi-year contracts with flat annual payments technically require you to pick a method, but since all methods yield the same answer, there's no ambiguity.

Step 4. Calculate the remaining components needed for the contracted ARR equation

We could have included the calculation of the three remaining values—: contracted expansions, contracted downgrades, and known churn—in the contracted ARR equation as separate steps.

All of them are pretty straightforward compared to calculating your annualized new bookings, though, especially if you're working with multi-year contracts with revenue that varies annually across the term of the contract. So, let’s run through each of them now.

Contracted expansions

Contracted expansions represent the annualized value of committed upsells, seat additions, or tier upgrades from existing customers that have been contracted but not yet implemented. In other words, expected revenue has not yet been added to the Current ARR.

What to include:

- Signed contract amendments for seat additions

- Committed tier upgrades ("Basic" to "Premium" to "Enterprise", for example)

- Add-on modules or features already contracted

- Geographic expansion commitments (adding new regions)

- Volume-based expansions with signed commitments

Notice that all of these represent known commitments. Any expansions without signed contracts should not be included in contracted ARR.

Contracted downgrades

Contracted downgrades reflect the annualized value of expected reductions in recurring revenue from existing customers that haven't been implemented yet. The revenue isn't reflected in Current ARR because the customer hasn't yet used the product for that portion of the contract and has formally indicated that there is no intention to do so.

This includes:

- Signed amendments reducing seat count

- Committed tier downgrades

- Removal of modules or features per signed agreement

- Geographic reductions (exiting specific regions)

- Volume reductions with signed commitments

Here's the formula to use for calculating contracted downgrades:

Known future churn

Known future churn represents the annualized recurring revenue from customers who have provided definitive notice of cancellation or whose contracts are expiring without renewal. These are still active customers and contributing to Current ARR.

What to include:

- Customers who have given formal termination notice

- Expiring contracts where the customer has confirmed non-renewal

- Customers in a wind-down period with a confirmed end date

- Contracts ending due to M&A activity (customer was acquired and the new company is not continuing the contract)

- Bankruptcies or business closures with known end dates

As with contracted expansions and downgrades, the formula for calculating known future churn is simple:

Step 5. Calculate contracted annual recurring revenue

At this point, you have all the values you need to calculate contracted ARR. Here's that formula one more time:

This step is simple. Plug in your numbers, and you're done. But you shouldn't stop there.

If you are one of the many businesses that need to normalize your annualized new bookings for this calculation, it's important to document your policy and processes for consistency and to make sure you can answer any hard questions that come your way when reporting your contracted ARR.

Step 6. Document your normalization policy

Record which normalization approach you used and why. And, make sure everyone on the finance team has access to that policy so they can consistently apply it over time.

For example, you could say something like: “We use the average approach for external reporting and provide first-year values for sensitivity analysis.”

Consistency matters for tracking trends over time, and transparency matters for stakeholder trust.

Common mistakes and challenges with contracted ARR

Getting contracted ARR right requires clean data and clear processes. Here's where companies commonly stumble:

- Sloppy CRM management: If your bookings data isn't well tracked, your contracted ARR calculation will be unreliable from the start. Contracts need to be logged accurately with correct values, start dates, and term lengths. If not, it'll end up following the well-known rule "garbage in, garbage out".

- Weak revenue recognition foundations: You need solid revenue recognition practices in place before contracted ARR becomes meaningful. If your team isn't clear on when and how revenue should be recognized, the distinction between "contracted" and "live" gets murky fast.

- Variable revenue without minimum commitments: Deals with variable pricing, tiered services, or usage-based billing complicate contracted ARR calculations. If there's no minimum revenue commitment in the contract, there's nothing concrete to include. You can't track what isn't guaranteed. Consider investing in tools that can handle this complexity if variable pricing is a significant part of your business.

- Customer Success teams not tracking known churn: Accurately forecasting churn is a common challenge. If your CS team isn't systematically documenting cancellation notices and non-renewals, the “known future churn" component of your contracted ARR will be incomplete. You need a system for tracking and analyzing churn to anticipate its impact.

- Misinterpreting contract terms: Not all contracts contribute equally to contracted ARR, especially those with varying lengths or payment schedules. It is important to carefully review each contract to determine the correct revenue recognition period and annual value. A three-year deal with heavy back-end loading looks very different from one with equal annual payments.

Why contracted ARR requires a unifying system

Contracted ARR is only as good as your operational discipline in maintaining it. While the formula is straightforward, keeping the underlying data accurate is hard—especially with multi-year contracts, varying annual commitments, and multiple teams touching the numbers.

Spreadsheets can work early on, but most finance teams need more sophisticated tools as they scale. Without good systems and governance, things fall apart quickly:

- Sales adds new bookings immediately after signing.

- Customer success forgets to subtract known churn.

- Finance isn't tracking contracted downgrades.

The result? Contracted ARR becomes inflated and unreliable.

You can avoid these problems with Drivetrain, an AI-powered FP&A platform built for the complexity of calculating and tracking contracted ARR at scale.

Drivetrain connects all your disparate systems—CRM, billing/revenue, and customer success platform—and automates both data flow and calculations. With 800+ native integrations, you can get connected in minutes with no manual uploads required.

Drivetrain handles everything from 50 contracts to 5,000, regardless of structure. It automatically calculates and tracks all intermediary values, updates in real time when source systems change, and with Drive AI providing continuous monitoring of your data pipelines and anomaly detection alerts, you’ll know instantly when outliers appear.

Book a demo today to see how Drivetrain can help you track and calculate contracted ARR without manual effort.

FAQs

Monthly at minimum, though many companies also track it quarterly and annually to evaluate period-over-period growth rates. However, the key is consistency.

Tracking contracted ARR at regular intervals lets you spot trends in bookings velocity, conversion rates, and churn before they become problems. Platforms like Drivetrain make this easier by pulling data from your CRM and billing systems automatically, so you're not rebuilding the calculation from scratch each month.

Bookings measure total contracted revenue in a period, including one-time fees, professional services, and the full contract value of multi-year deals, whereas contracted ARR is narrower.

It only includes recurring revenue, normalized to an annual value. A $300K three-year deal counts as $300K in bookings but contributes far less to contracted ARR depending on how you normalize it. Think of bookings as what you sold; contracted ARR represents what that translates to in annualized recurring revenue.

Contracted expansions get added to contracted ARR as soon as the amendment is signed and not when it goes live. Use the incremental annual value, not the total contract value.

For usage-based expansions without contractual commitments, only include the committed minimum. Anything beyond that is upside, not guaranteed revenue. It's worth tracking expansion contracted ARR separately so you can monitor upsell effectiveness over time.

Use ARR to establish your current baseline because it represents recognized, billing revenue. Use contracted ARR to demonstrate forward visibility and growth trajectory.

Just be clear about which metric you're presenting, as investors increasingly ask whether stated figures are "contracted" or "live," and conflating the two erodes credibility. Present both, explain the gap, and show your historical conversion rates to give stakeholders confidence that contracted revenue actually converts.

First-year values are the safer choice for external reporting as they reflect near-term revenue reality and reduce the risk of overstating growth to investors or your board.

For internal forecasting and capacity planning, some teams use averaged values across the contract term.

The use of exit-year values is highly discouraged because they can materially overstate current revenue potential, especially for contracts with heavy back-end loading or ramped deployments.

Like this article?

.svg)

.svg)

.svg)

%20Header.svg)